In the second of this two-part look at Blackpool FC's finances from the financial year ending May 31 2010 we'll examine more of how the club has conducted its business, and how the influx of Premier League money will impact the club in the future. Last time out we focused on:

- Ownership

- Losses and Negative Net Worth

- Increasing Turnover

- Stadium Development

Before continuing with this article, I would advise that you first read part one, which can be found here. This time round I'd like to examine the following:

- Player Wages

- Debt

- Influx of Premier League Money

- The Future

Player Wages

As with most items in the club's accounts, it's impossible to isolate the exact information for wages for the playing staff, but it can be reasonably assumed that they form the majority portion of wages listed in the accounts. The chart below shows wages for the last four years (N.B £5m has been deducted from the 09/10 wages - the reported value of the promotion bonus - as it would unfairly skew the results)

{kind=link}

Even after the £5m promotion bonus is deducted from the wages in 09/10, it can be seen that the wage bill was on a steady rise following promotion from League One, but the jump from 08/09 to 09/10 was almost double that of the rise from 07/08 to 08/09. Charlie Adam's wages no doubt played a part here, just as the other high profile signings would have - Hameur Bouazza, Neal Eardley, Seamus Coleman (loan) and even Jason Euell are likely to have been earning more than comparable players from the previous season. When you also consider the performance-related pay that is widely reported to have been built into many of the players' contracts, an increase in win and goal bonuses is an inevitable side-effect of a promotion season. It can't be said that Blackpool gambled on winning promotion in the vein of other clubs, but in 09/10 they did perhaps extend themselves to their limit.

A common way of assessing if clubs are spending too much on wages is to compare this cost against turnover. While there are no caps in top divisions for what percentage of a club's turnover can be spent on wages, anything much above 70% can be considered a little high - League Two operates a scheme whereby clubs have to limit this ratio to 60%.

In the four years shown, the arrival of Valeri Belokon before the 06/07 season saw 'Pool throw a decent amount of money (by their own standards) at a successful promotion push, with the increased turnover of Championship football in 07/08 bringing the ratio down the following year. 08/09 saw Blackpool rely heavily on the loan market, resulting in a ratio around the 75% mark and the ratio for 09/10 remained relatively static, despite the 35% increase in turnover. Had the Seasiders not won promotion, Blackpool would surely have tried to reduce this ratio, although defeat at Wembley would have surely signalled the departure of Charlie Adam for a not insignificant transfer fee anyway, in turn affecting the wages.

One would anticipate that this ratio will drop dramatically on the 10/11 accounts, with a sharp increase in turnover as part of the Premier League's huge television revenue.

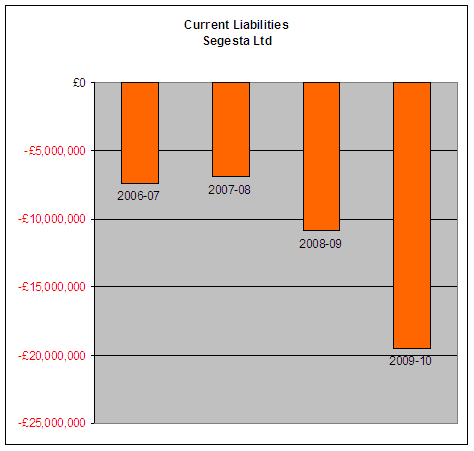

That the club has been operating with a level of debt is nothing unusual in the football industry, but how much the club owes, and to whom, is a rather more complex issue. We have already established in part one that much of the club's accounts portray a misty picture, and the same can be said of how the debts are illustrated. The group's total liabilities over the last four years are shown below.

The group's total debt has obviously sharply increased from 2008/09 (£15.4m) to 2009/10 (£27.2m), but in order to understand this it is necessary to drill down into the debt in more detail. Creditors are separated into two categories in the accounts - debts due within one year (current liabilities) and debts due after more than one year (long-term liabilities). First we'll analyse the current liabilities - these are shown below.

An increase in the group's current liabilities from £10.9m to £19.4m at first seems alarming, but on closer examination isn't perhaps so bleak, not least because the incoming Premier League money dwarves this figure. Included in the current liabilities is the aforementioned £5m promotion bonus, which while accrued during the 09/10 season was infamously not paid until August 2010, much to the chagrin of the playing staff who got the PFA involved to settle the dispute.

The group's total debt has obviously sharply increased from 2008/09 (£15.4m) to 2009/10 (£27.2m), but in order to understand this it is necessary to drill down into the debt in more detail. Creditors are separated into two categories in the accounts - debts due within one year (current liabilities) and debts due after more than one year (long-term liabilities). First we'll analyse the current liabilities - these are shown below.

An increase in the group's current liabilities from £10.9m to £19.4m at first seems alarming, but on closer examination isn't perhaps so bleak, not least because the incoming Premier League money dwarves this figure. Included in the current liabilities is the aforementioned £5m promotion bonus, which while accrued during the 09/10 season was infamously not paid until August 2010, much to the chagrin of the playing staff who got the PFA involved to settle the dispute.

Elsewhere current liabilities exist in the form of a loan from Protoplan Limited - an Owen Oyston-owned company - in excess of £4m. It is unclear what the purposes of this loan was - Protoplan is listed as a 'building completion' firm - but the accounts state this was repaid in full on 17th September 2010, no doubt once the first tranche of Premier League money had been received.

Another Oyston backed company is also owed money by the club - Zabaxe Limited - and the story surrounding this debt is not straightforward either. Zabaxe is owed in the region of £944k, a debt stretching back more than a decade. In 2000 this debt was converted to share capital in Segesta Limited, but in the past financial year this transaction was deemed to be avoided - essentially it has been decided that for whatever reason this should not have been allowed. Therefore the original debt has been reinstated, and the share capital reduced. The accounts state that this debt of £944k was due to be paid in 2010/11.

An increase in trade creditors - other football clubs - due within the next year has also increased by around £800k with the various transfers, which are often paid in installments. The club has also called upon Valeri Belokon's Baltic International Bank for a loan of £800k at an interest rate of 8%, which was due to be repaid on June 30th 2010. A separate loan for around £500k was received in the financial year from Belokon's VB Football Assets Ltd, which one would expect was the vital contribution which secured the signing of Charlie Adam. This particular loan has also been repaid since the turn of the financial year, specifically on 2nd December 2010.

Albeit not an external creditor, Blackpool Football Club Limited continues to repay a debt to the parent company Segesta Limited at a rate of £435k per year - the amount receiver from the occupiers of the North and West stands, less a 10% administration fee. As of 31st May 2010, the remaining debt stood at £2.7m. Repaid at the current rate it will be cleared in six years, but whether the influx of Premier League money might see the parent company recoup the debt more quickly remains to be seen.

Looking to the longer term, the chart below shows the group historical long term liabilities.

The bulk of the long term liabilities during 08/09 was comprised of the loan owed to Protoplan, and with that becoming a current liability in 09/10, and now paid of as of September 2010, the long term debt in the 09/10 accounts comes from a different source.

Almost £7.5m is owed to Blackpool's Latvian investor, in one form or another. Two significant outstanding loans remain - one of £4.75m to Valeri Belokon's VB Football Assets Limited, and the other a £2.7m loan to Miss Vlada Belokon, the Club President's daughter. One can only speculate why this personal loan comes from his daughter and not Mr Belokon himself, but it does show the influence the Latvian investment has had on the club. According to the club's accounts, it is intended that these loans will be repaid from revenue received from the South and South West corner, suggesting that it was indeed Valeri Belokon who put up the money to get the stadium improvements back on track.

A personal loan in the region of £275k is also owed to Owen Oyston, but it is unclear how and when this loan will be repaid. The accounts state that Mr Oyston will not seek repayment in the current financial year, but with money flooding into the club's coffers following promotion, it wouldn't necessarily be a surprise to see this debt cleared sooner rather than later - the same might also be said for the loans to the various Belokon-related creditors.

Overall the club's debts, albeit a little complex, won't be giving anyone any sleepless nights. The incoming Premier League money ensures that the clubs are in a fine position to meet their debts as they fall due, and if the club wants to loosen its shackles, can even pay them off early. The fabled £90m figure for one season in the Premier League and four years of parachute payments will, if nothing else, mean that the club is virtually debt-free going forward - an achievement not to be underestimated in the current climate. Once the debts to the Oyston and Belokon families are cleared, this would also surely mean that the club can really start to benefit from the various letting units in the stadium, on top of its football income.

Another Oyston backed company is also owed money by the club - Zabaxe Limited - and the story surrounding this debt is not straightforward either. Zabaxe is owed in the region of £944k, a debt stretching back more than a decade. In 2000 this debt was converted to share capital in Segesta Limited, but in the past financial year this transaction was deemed to be avoided - essentially it has been decided that for whatever reason this should not have been allowed. Therefore the original debt has been reinstated, and the share capital reduced. The accounts state that this debt of £944k was due to be paid in 2010/11.

An increase in trade creditors - other football clubs - due within the next year has also increased by around £800k with the various transfers, which are often paid in installments. The club has also called upon Valeri Belokon's Baltic International Bank for a loan of £800k at an interest rate of 8%, which was due to be repaid on June 30th 2010. A separate loan for around £500k was received in the financial year from Belokon's VB Football Assets Ltd, which one would expect was the vital contribution which secured the signing of Charlie Adam. This particular loan has also been repaid since the turn of the financial year, specifically on 2nd December 2010.

Albeit not an external creditor, Blackpool Football Club Limited continues to repay a debt to the parent company Segesta Limited at a rate of £435k per year - the amount receiver from the occupiers of the North and West stands, less a 10% administration fee. As of 31st May 2010, the remaining debt stood at £2.7m. Repaid at the current rate it will be cleared in six years, but whether the influx of Premier League money might see the parent company recoup the debt more quickly remains to be seen.

Looking to the longer term, the chart below shows the group historical long term liabilities.

The bulk of the long term liabilities during 08/09 was comprised of the loan owed to Protoplan, and with that becoming a current liability in 09/10, and now paid of as of September 2010, the long term debt in the 09/10 accounts comes from a different source.

Almost £7.5m is owed to Blackpool's Latvian investor, in one form or another. Two significant outstanding loans remain - one of £4.75m to Valeri Belokon's VB Football Assets Limited, and the other a £2.7m loan to Miss Vlada Belokon, the Club President's daughter. One can only speculate why this personal loan comes from his daughter and not Mr Belokon himself, but it does show the influence the Latvian investment has had on the club. According to the club's accounts, it is intended that these loans will be repaid from revenue received from the South and South West corner, suggesting that it was indeed Valeri Belokon who put up the money to get the stadium improvements back on track.

A personal loan in the region of £275k is also owed to Owen Oyston, but it is unclear how and when this loan will be repaid. The accounts state that Mr Oyston will not seek repayment in the current financial year, but with money flooding into the club's coffers following promotion, it wouldn't necessarily be a surprise to see this debt cleared sooner rather than later - the same might also be said for the loans to the various Belokon-related creditors.

Overall the club's debts, albeit a little complex, won't be giving anyone any sleepless nights. The incoming Premier League money ensures that the clubs are in a fine position to meet their debts as they fall due, and if the club wants to loosen its shackles, can even pay them off early. The fabled £90m figure for one season in the Premier League and four years of parachute payments will, if nothing else, mean that the club is virtually debt-free going forward - an achievement not to be underestimated in the current climate. Once the debts to the Oyston and Belokon families are cleared, this would also surely mean that the club can really start to benefit from the various letting units in the stadium, on top of its football income.

Influx of Premier League Money

Returning to football income, the latest set of published accounts paint a story far removed from the current situation Blackpool FC finds itself in. With the prestige of top flight football comes the riches to match, and the levels of turnover the club will achieve this season will be by far the highest in its history. Exact figures are naturally difficult to come by but Blackpool FC appears to have timed promotion at a lucrative moment. Not only is the Premier League in the first year of an improved television deal, parachute payments have also been increased in the worst case scenario of relegation.

The amount of television revenue each club receives is calculated on the following basis:

- 50% - Basic Award

- Each club receives an equal share of half of the television revenue, for both domestic and international rights.

- 25% - Facility Fees

- For each game shown on live TV, clubs are awarded a facility fee. Typically this is a minimum of 10 games for each team (although Blackpool look set to feature in just nine televised fixtures). Naturally, the more often a club features, the larger its share of the payments.

- 25% - Merit Payments

- Clubs receive a payment based on their final league position. Last year the payment for finishing in 20th was around £800k, with a further £800k for each place above that, up to a total of £16m for winning the title.

The new system for parachute payments ensures a total of £48m over the course of four seasons, assuming promotion back to the top flight is not attained. This is paid in sums of £16m for the first two years, with that figure halving for the remaining two seasons. Averaged out at £12m a season, this still eclipses total revenue from any previous years. With contracts reported to contain clauses that see wages drop upon relegation, from already modest salaries, the club would appear to still be in a healthy position whatever the outcome of this season - in a financial sense at least.

The Future

Of course, before we even contemplate Blackpool FC's financial future beyond the end of this season (whatever division that may be in) there are some obvious events which have taken place after the publication of the accounts being analysed in this article. Off-the-field, the new East Stand is sure to make an impact on the 2010/11 accounts, as is the continued fit-out of the South Stand. On the playing side of things some higher transfer fees are inevitably going to have to be considered. Although meagre by Premier League standards, it's likely that Blackpool may have spent as much as £5m, although the fees will be accounted for over the length of the players' contracts. Wages too will have risen considerably, possibly to more than double the previous season's level - and a potential survival bonus of another £5m will drive this even higher.

The Seasiders should turn a tidy profit in 2010/11, but when the various costs above are considered, as well as the various debt pay-offs, it may not be quite as profitable a year as some may have expected. Ultimate reward comes from a sustained spell in the Premier League but the club is in a healthy state and as already discussed, could see itself become almost debt-free within the next couple of years - an enviable position for every other football club out there.

This is not to say that all is rosy in the garden - key concerns will remain among the Blackpool support and with good reason. One supposed benefit of earning promotion, alongside the redevelopment of Bloomfield Road, was meant to be a brand new training ground. However, almost one year on this seems no nearer to reality and one wonders if the idea will be shelved completely if the worst happens and the club are relegated this May. It cannot be denied that the surroundings the players work in can be an important factor in attracting new talent, in both transfers for the first team and at youth level. A more professional training set-up is surely key to Blackpool establishing itself as a club that belongs in the top flight.

Another consequence of relegation could be a possible lack of competitiveness. Given the financial gulf that continues to widen between the Premier League and the Championship, any relegated team should normally be expected to throw its weight around and compete at the very top with their financial clout. However, a drop in wages upon relegation would likely see Blackpool return to an average-sized Championship wage bill at best. 'Pool proved in 09/10 that wages aren't always the key factor, but that promotion bid must surely be the exception rather than the rule. The club may have a healthy profit & loss account whatever division they find themselves in next season, but fans will undoubtedly worry about the ambition of an immediate return.

For now, all of this talk is hypothetical. Blackpool FC's financial future is stable, but the next couple of months will decide whether the club can kick on from this position, or merely use the Premier League money to consolidate themselves as a competitive Championship side. Either of those options would have been a dream only five years ago, but with around £50m riding on the outcome of this season, the pressure (like it or not) is well and truly on.

Excellent read....

ReplyDelete'Promenade Developments Limited' is actually registered as 'Promenade Developers Limited' Puzzle solved. But keep digging. Eventually you WILL dig up the bodies.

ReplyDeleteFreeholds? Rents? Any answers? Not academic.

ReplyDeleteAstounding what the power of money can make a man do. A secret labrinyth of companies all throwing money at each other and all belonging to the one man. Take a bow the elusive Mr O.

ReplyDeleteThanks again mate - another interesting read.

ReplyDeleteAll very interesting but as Inspector Clouseau would say "You zink I know nozzink. I tell you, I know b**ger all". So explain to a dummy, does the football club (the playing side) own the ground? If not, who or what does? What was the purpose of all the multitude of loans? Why is that so difficult to find out from the accounts? If they were 'family and friends' lenders, why such high rates of interest. Not exactly 'friendly' are they? If Pool go down, no doubt the fans will start to take an interest in the finances when money is not forthcoming to replace Charlie, David,DJ etc etc. Right now survival is all.

ReplyDelete